Table of Content

You’ll want to keep closing costs in mind when refinancing a loan, as they can add up to thousands of dollars. Before you decide to refinance, divide your closing costs by how much you expect to save every month by refinancing to see if it’s worth it. While your lender can advise you on the costs and benefits of the transaction, you’ll want to be sure you understand what you’re getting into. Consumer Financial Protection Bureau , the average VA loan closing costs in 2021 were $8,391, while the average VA loan was valued at $354,474.

When you're planning to get a VA loan, be sure to factor closing costs into the equation. That said, they may not all fall on you; there are ways you can potentially avoid having to pay some of these fees. Closing costs typically end up falling somewhere between 3% and 5% of the total loan amount.

Application Fee

The larger the down payment you make, the funding fee will represent a smaller percentage of the loan. When you’re using a different type of loan, you will likely face attorney fees from the lender and settlement charges. “Closing costs” is a broad term used to define a wide range of fees you’ll encounter through the closing process, including your home appraisal and the title search.

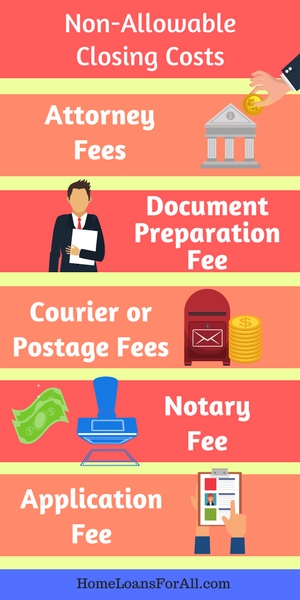

Andrew Dehan is a professional writer who writes about real estate and homeownership. Based on the information you have provided, you are eligible to continue your home loan process online with Rocket Mortgage. This is the standard insurance policy that protects against perils like fire, trees falling on the home, tornadoes or other natural disasters. Note that the VA does not permit the veteran to pay an attorney for anything besides title work. VA borrowers, however, weren’t able to obtain appraisals virtually, resulting in late reports that put transactions at risk.

Third-party fees

She co-created the 30 Day Immune System Challenge at 30ichallenge.com. Information provided on Forbes Advisor is for educational purposes only. Your financial situation is unique and the products and services we review may not be right for your circumstances.

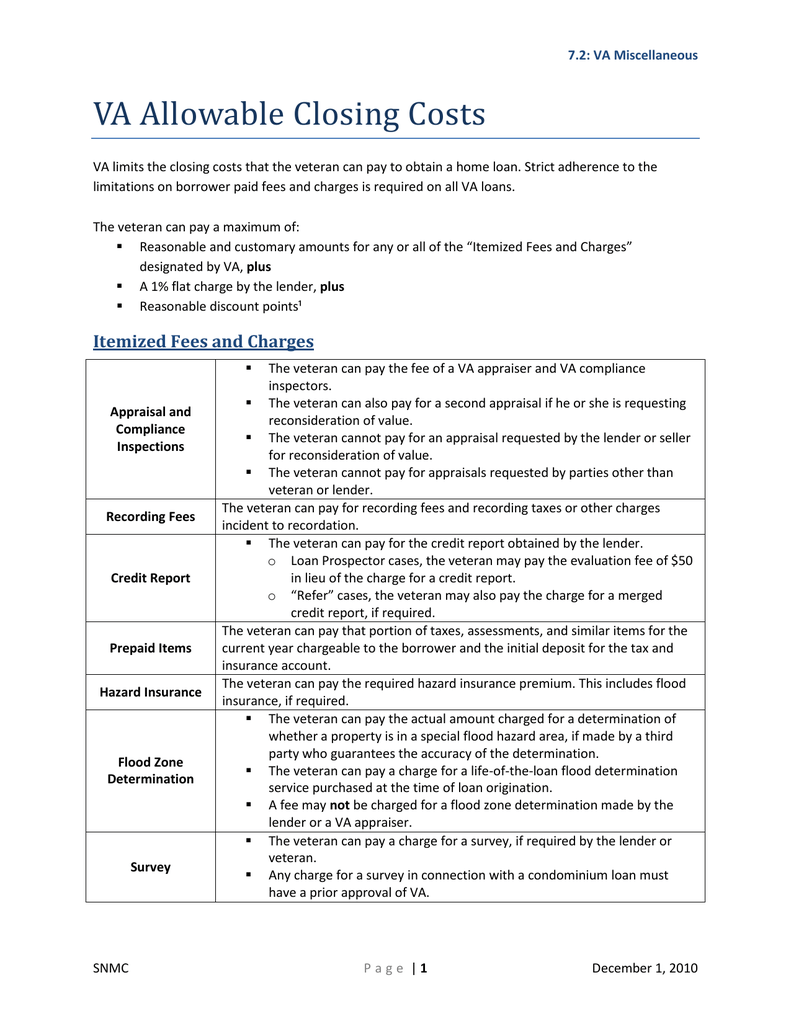

Borrowers will not be charged more than 1% of the total loan amount as an origination fee when using a VA loan. Typically, mortgage loan origination fees range from 0.5 – 1% of the total loan amount. So, this limited origination fee is in line with what you might pay with a different type of mortgage loan. Homebuyers are responsible for paying closing costs, but they can ask for help from the seller who is allowed to pay up to 4% of the loan amount toward closing costs. Closing cost assistance programs and lender credits can also help.

How Much are VA Closing Costs?

The lender will pull a flood certification, or “flood cert,” on the property to determine whether it’s in a flood zone. But if yours is, you will need to purchase flood insurance (see “Prepaid Items” section below). The title report and title insurance protect the lender and owner of the home in case someone claims ownership rights to the house, and wins in a court of law. If that were to happen for any reason, the title insurance company would reimburse the lender and owner of the home for the loss. If you are using a VA streamline to refinance your home, an appraisal is not required and this fee will not apply. If your lender is requiring an appraisal on a VA streamline refinance, shop around for another lender.

Again, they’re not required to pay any of them, so this will always be a product of negotiation between buyer and seller. It's not unusual for buyers to work with their agents to negotiate for sellers to pay certain closing costs. Buyers can ask the seller outright to pay these costs and fees from the sale proceeds.

It could also make it harder for you to get enough money out of the future sale of the home to pay off your loan balance. In a buyer's market, where demand is low and supply is high, you'll have more leverage. You could make an offer requiring the seller to cover some of the closing costs. But in a competitive market, this tactic won't likely go over well.

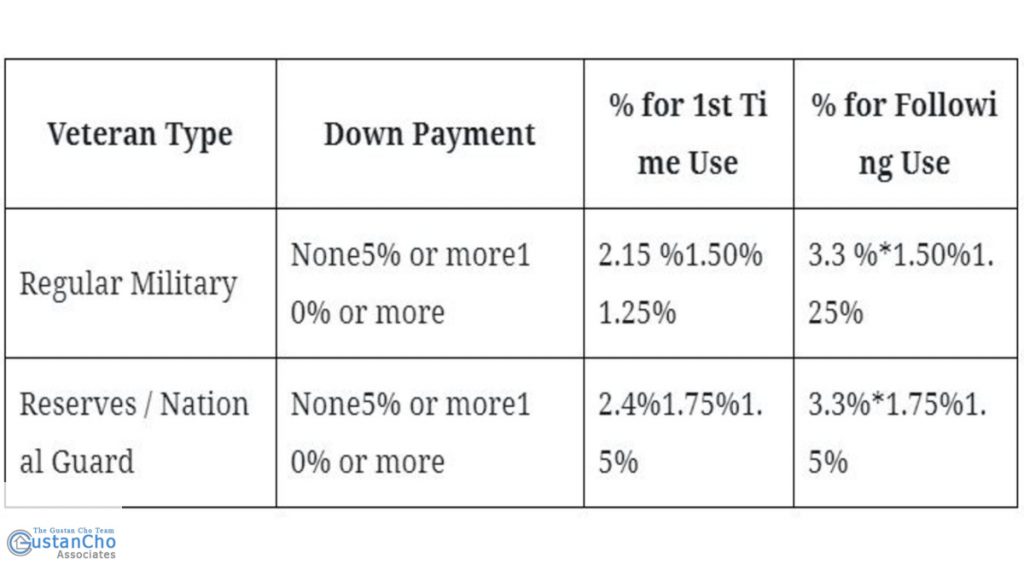

Some fees are not allowed to be charged, per VA loan program guidelines. Repeat homebuyers pay higher fees, but refinances through the VA’s Interest Rate Reduction Refinance Loan require only a 0.5% funding fee. You can also pay a lower fee by making a down payment of 5% or higher.

For instance, New York’s fee is $625 for a single family home or condominium, and North Carolina’s high demand counties have a fee of $800. If you’re taking out a $300,000 home loan, each discount point will cost you $3,000 up front, for which you’ll receive a discount on your interest rate of 0.25%. If your VA loan requires it, you may have to pay for a land survey. As the buyer, you can also request a survey of the land even if your loan doesn’t require it. If your lender requests a survey for a condominium loan, they must have the prior approval of the VA.

They cover everything from the lender’s administrative fees to getting a head start on next year’s property taxes and insurance premiums. Closing costs — also called closing fees — include a variety of charges that make buying a house possible. If you’re on the fence about refinancing, a simple calculation can help you determine how long it will take you to recuperate your closing costs. If the home you’re buying is in a neighborhood governed by an HOA, you’ll be responsible for monthly, quarterly or yearly dues. In addition to prorated dues based on your closing date, you may also have to pay a one-time initiation fee at closing. Review the VA funding fee rate charts below to determine the amount you’ll have to pay.

If you’re using a VA home loan to buy, build, improve, or repair a home or to refinance a mortgage, you’ll need to pay the VA funding fee unless you meet certain requirements. When you purchase a discount point on your mortgage, you’re essentially paying cash upfront to reduce the interest rate on your mortgage. Discount points save you money over the length of the loan, though each point is priced at 1% of the loan. This is called a “seller concession” and can include the VA funding fee.

No comments:

Post a Comment